A period prepared as a small company under FRS 102 Section 1A discloses much more than a micro-entity, and the Notes window grows to match — around thirty sections instead of four. The statements themselves change too: the balance sheet breaks out debtors, stock and cash, and each line can reference a numbered note.

Notes that fill themselves in

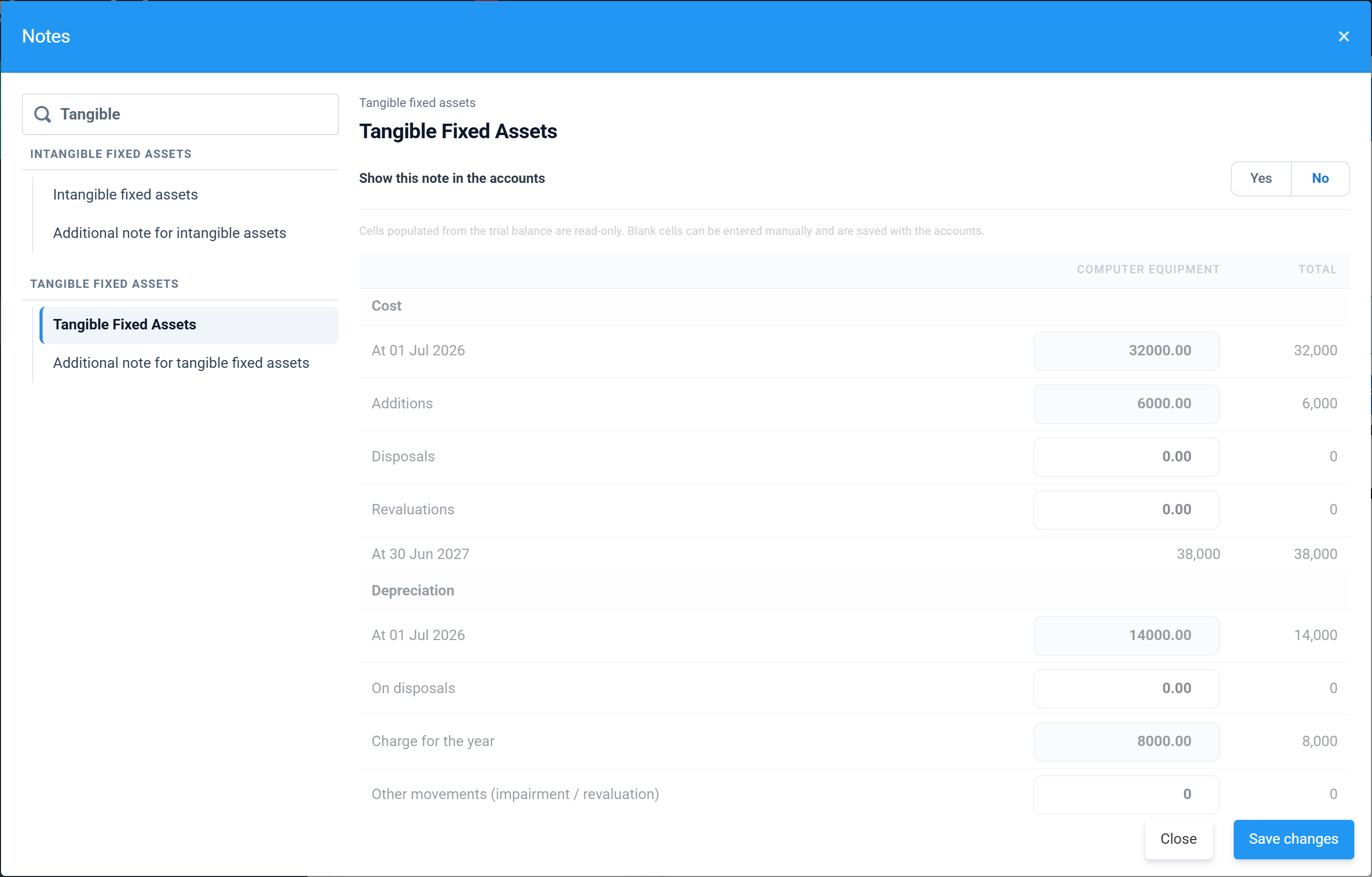

Wherever a note’s figures already exist in your trial balance, the editor shows them read-only — you can’t accidentally disagree with your own balance sheet. The Tangible fixed assets note builds its cost and depreciation movement table from the trial balance, leaving only the cells the trial balance can’t know (disposals, revaluations) open for entry:

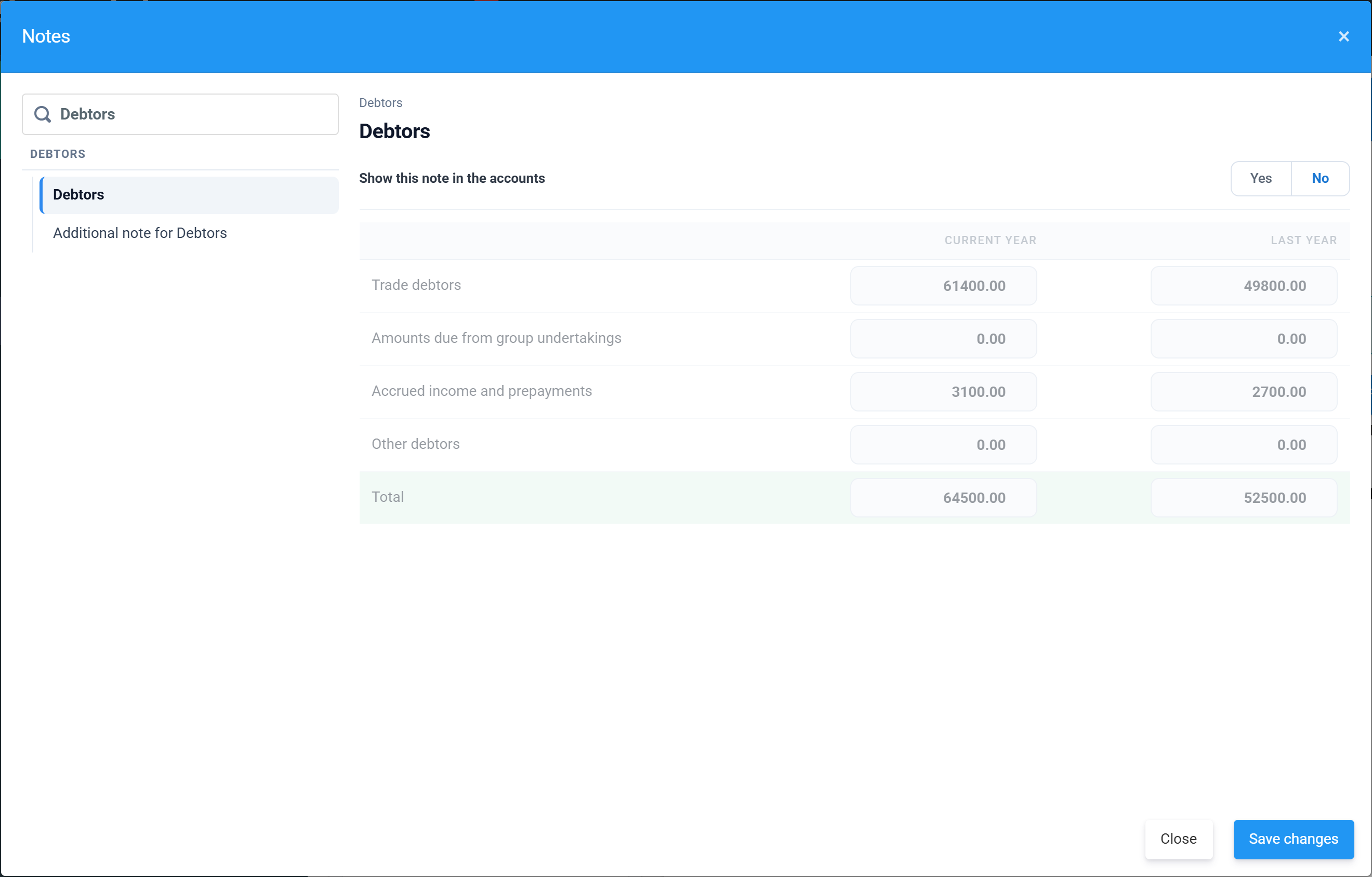

The Debtors note is built the same way, splitting trade debtors, amounts due from group undertakings, prepayments and other debtors:

The note groups, briefly

- Statutory information & compliance — the company’s legal details and the statement of compliance with FRS 102 1A. Usually template wording.

- Profit-and-loss notes — turnover (how revenue is measured), operating profit (what’s been charged in arriving at it), taxation and dividends.

- Asset notes — intangible and tangible fixed assets, investment property, investments, current asset investments and inventories. The movement tables draw from the trial balance as above.

- Debtors, creditors and provisions — debtors, creditors due within and after one year, deferred taxation and provisions for liabilities.

- Equity notes — share capital, capital contribution reserve, capital redemption reserve and company-limited-by-guarantee wording.

- Commitments and related parties — capital, pension and operating lease commitments, contingent liabilities, guarantees provided on behalf of directors, transactions with related parties, controlling party and events after the reporting date.

- Average number of employees — the same mandatory figure as FRS 105, with the same zero-count warning (see the FRS 105 article).

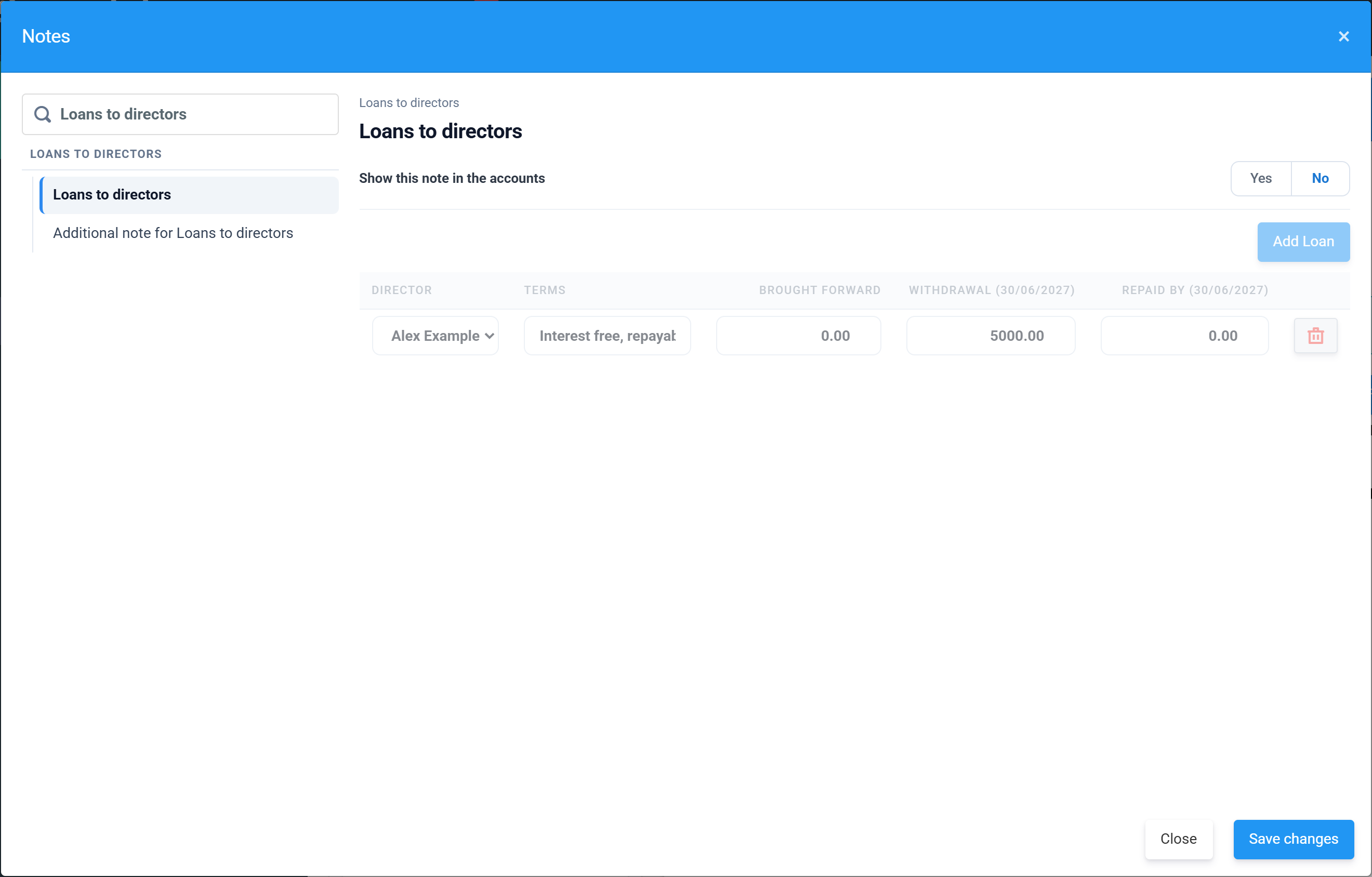

The Loans to directors note has its own small ledger — add a loan per director with its terms, brought-forward balance, advances and repayments in the year:

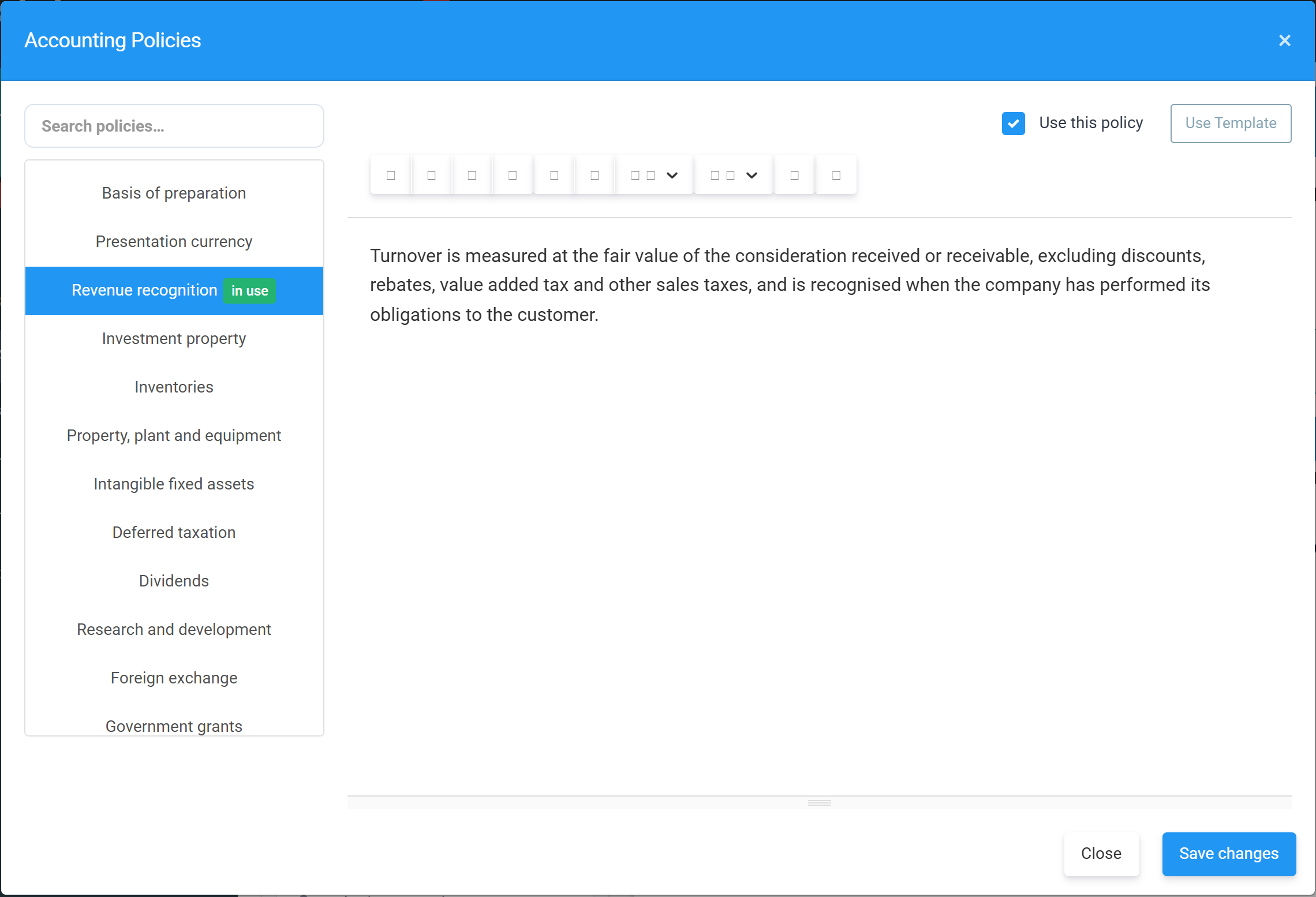

Accounting policies

FRS 102 1A accounts open their notes with the accounting policies the company applies. The Policies action (it only appears for FRS 102 1A periods) lists the standard policy headings — basis of preparation, revenue recognition, property plant and equipment, and so on. Tick Use this policy on the ones that apply and write (or template) the wording; policies marked in use print in the accounts in the order listed.

Next: the checks before you file — see Validation, signing and signed accounts.