Beta feature — Partnership (SA800) returns are currently in beta and are switched on for one accountant firm at a time. To gain access for your firm, email support@taxoptimiser.co.uk and the team will enable it and help you get started.

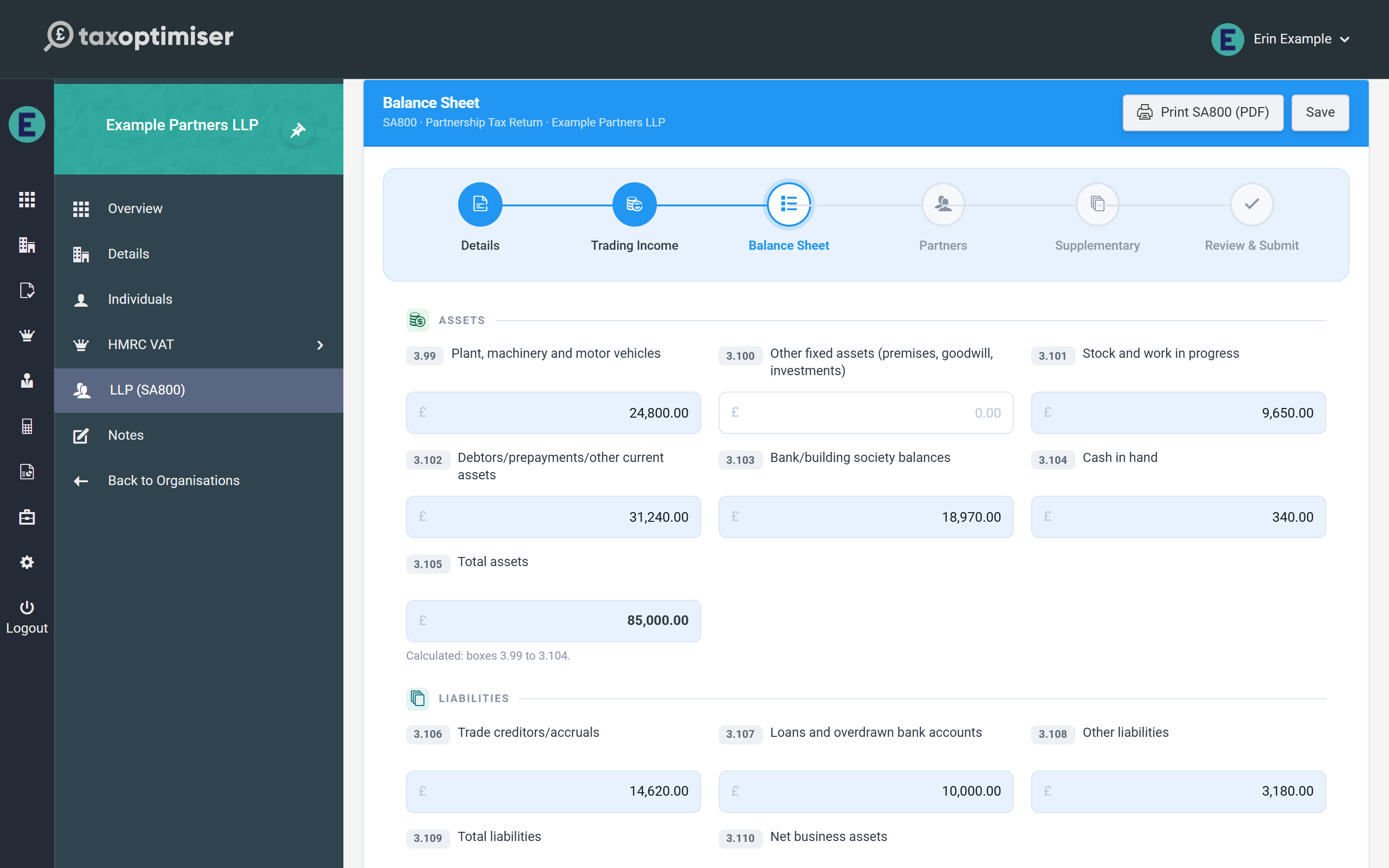

The Balance Sheet step covers the SA800’s summary balance sheet (boxes 3.99–3.115) — a condensed snapshot of the partnership’s position at the period end, with all three totals calculated for you.

Assets and liabilities

- Assets (3.99–3.104): plant, machinery and vehicles; other fixed assets; stock and work in progress; debtors and prepayments; bank balances; cash. Total assets (3.105) is calculated.

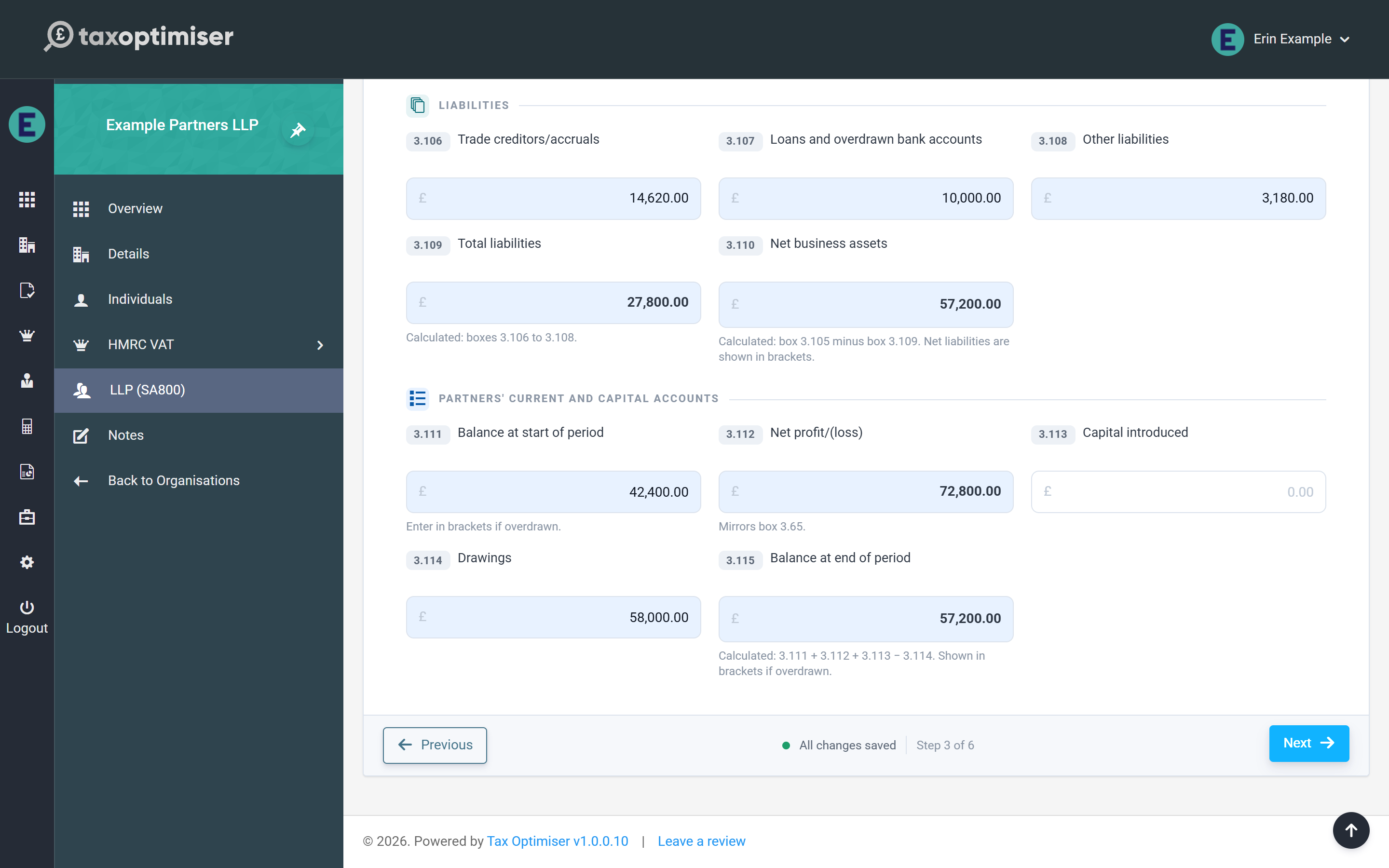

- Liabilities (3.106–3.108): trade creditors and accruals; loans and overdrawn bank accounts; other liabilities. Total liabilities (3.109) is calculated.

- Net business assets (3.110) — calculated as 3.105 minus 3.109; net liabilities show in brackets.

Partners’ current and capital accounts

The final group reconciles the partners’ combined accounts across the period:

- Balance at start of period (3.111) — enter in brackets if overdrawn

- Net profit/(loss) (3.112) — mirrors box 3.65 from the Trading Income step automatically

- Capital introduced (3.113) and drawings (3.114)

- Balance at end of period (3.115) — calculated: 3.111 + 3.112 + 3.113 − 3.114

A useful cross-check before moving on: on a balance sheet that balances, the closing balance in 3.115 equals net business assets in 3.110. If the two disagree, an asset, liability or drawings figure is missing or mistyped.

Next: the Partnership Statement — partners and profit shares.