Partnerships with income beyond the trade report it on the SA800’s supplementary pages. The Supplementary step gathers all four on one screen; a page is only included in the submission when it actually carries figures, and the Review step lists which pages will go (“Supplementary pages with data”).

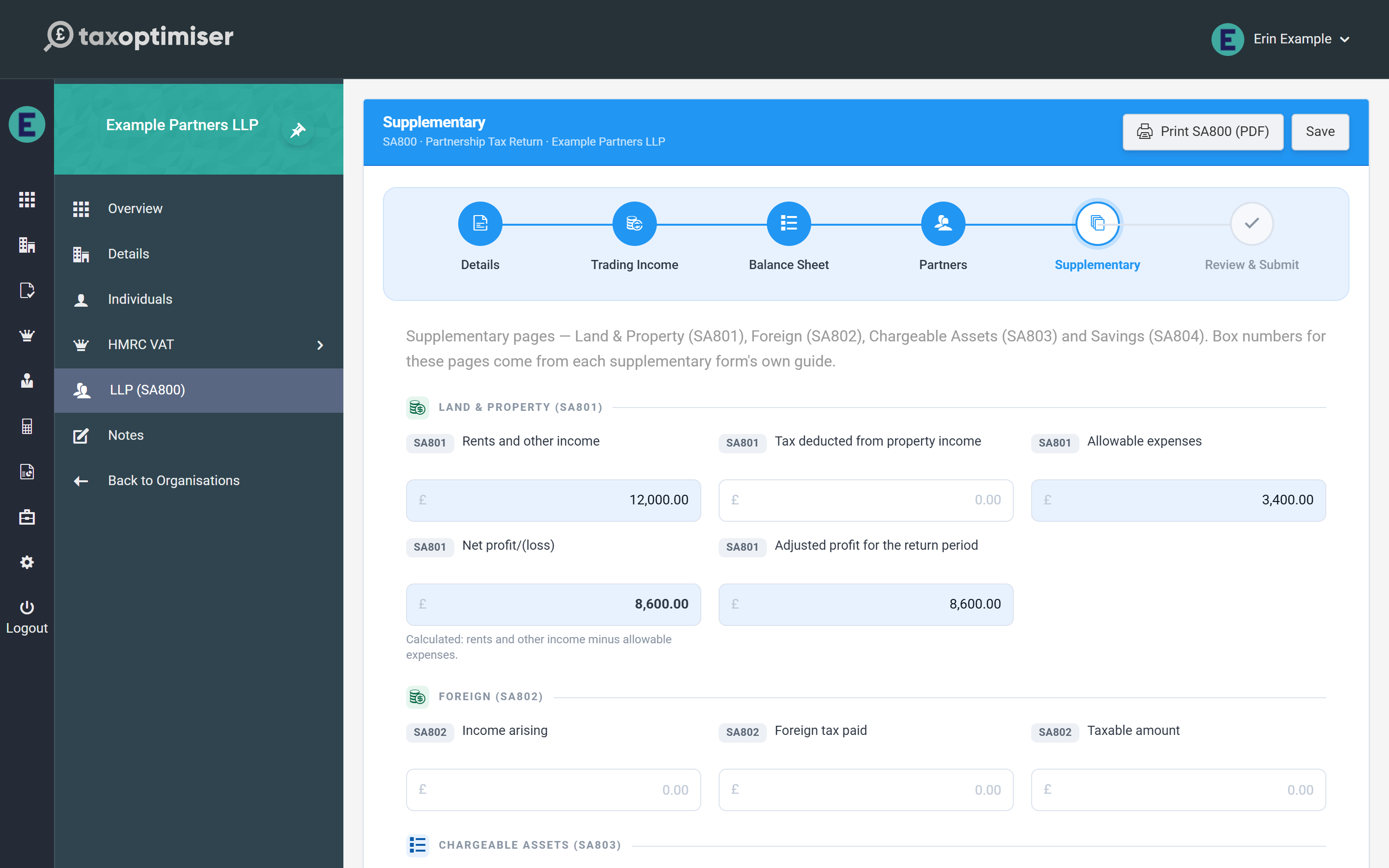

Land & Property (SA801)

Rental business income: rents and other income, any tax deducted from it, and allowable expenses. The net profit/(loss) is calculated (income minus expenses), and the adjusted profit for the return period carries any adjustments you compute.

Foreign (SA802)

Overseas income: the income arising, foreign tax paid on it, and the taxable amount.

Chargeable Assets (SA803)

The partnership reports only the disposal proceeds from chargeable assets sold in the period. That is deliberate — a partnership isn’t itself chargeable to capital gains tax, so each partner computes their own gain or loss on their share via their personal return.

Savings (SA804)

Investment income: untaxed UK bank and building society interest, gross (box 7.9A), tax deducted from savings income, and other savings income.

Like the main pages, anything the form derives is calculated read-only, and leaving a page untouched simply leaves it out of the filing — there is nothing to switch on or off.