Beyond the core income sections, the return’s supplementary pages each have their own entry in the section picker. As everywhere else, every box carries its HMRC reference badge, saves as you leave it, and feeds the live calculation immediately.

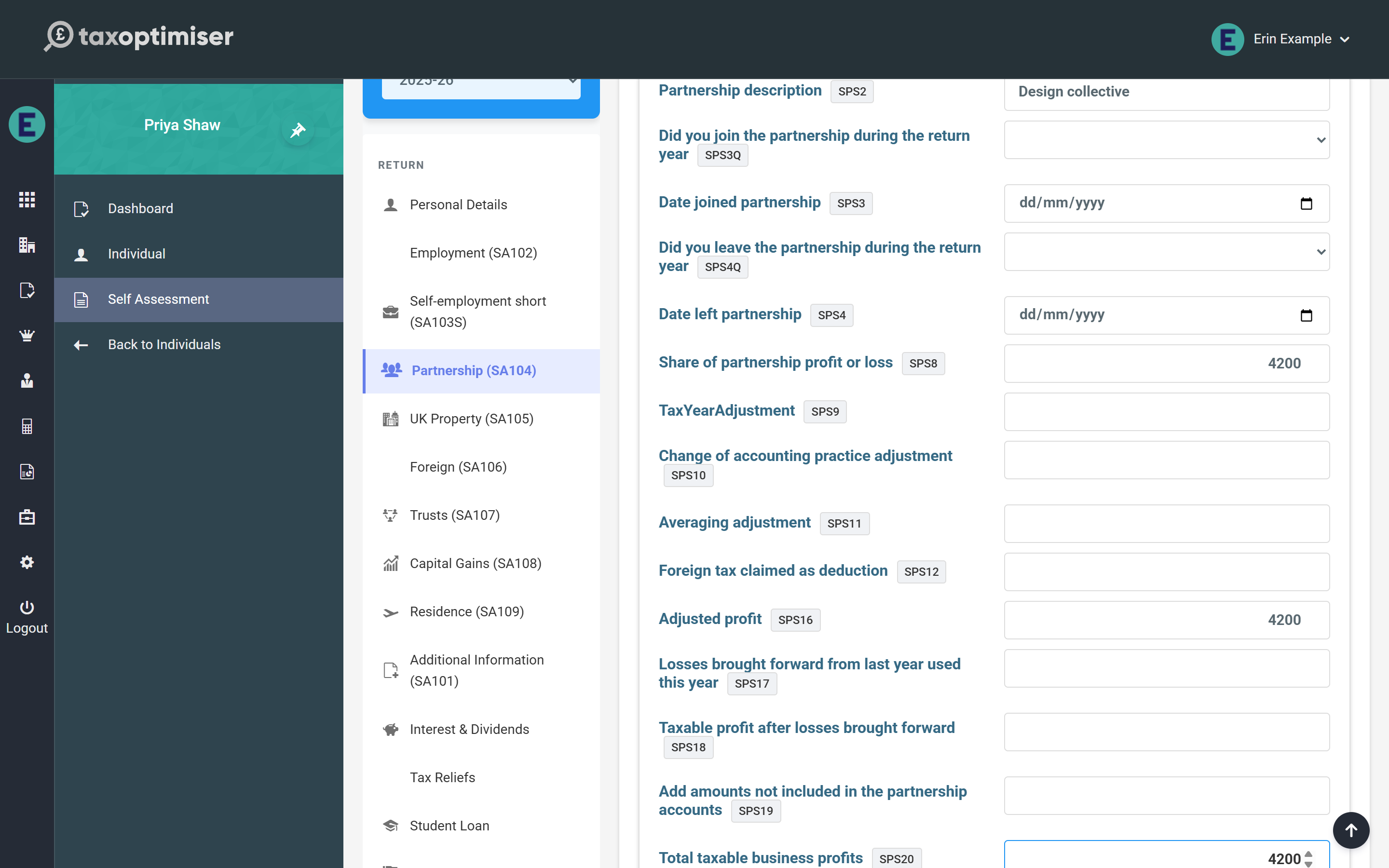

Partnership (SA104)

Choose short or full statements to match what the partnership issued, and press Add Partnership for each one — a client can carry any number, each in its own card titled by the partnership’s name. Enter the shares exactly as they appear on the partnership statement: the profit share flows into the calculation including Class 4 National Insurance (with the exemption tick and adjustment box honoured), voluntary Class 2 can be chosen here too, and the full statement adds the client’s shares of savings, dividend, property and other income plus any tax deducted at partnership level.

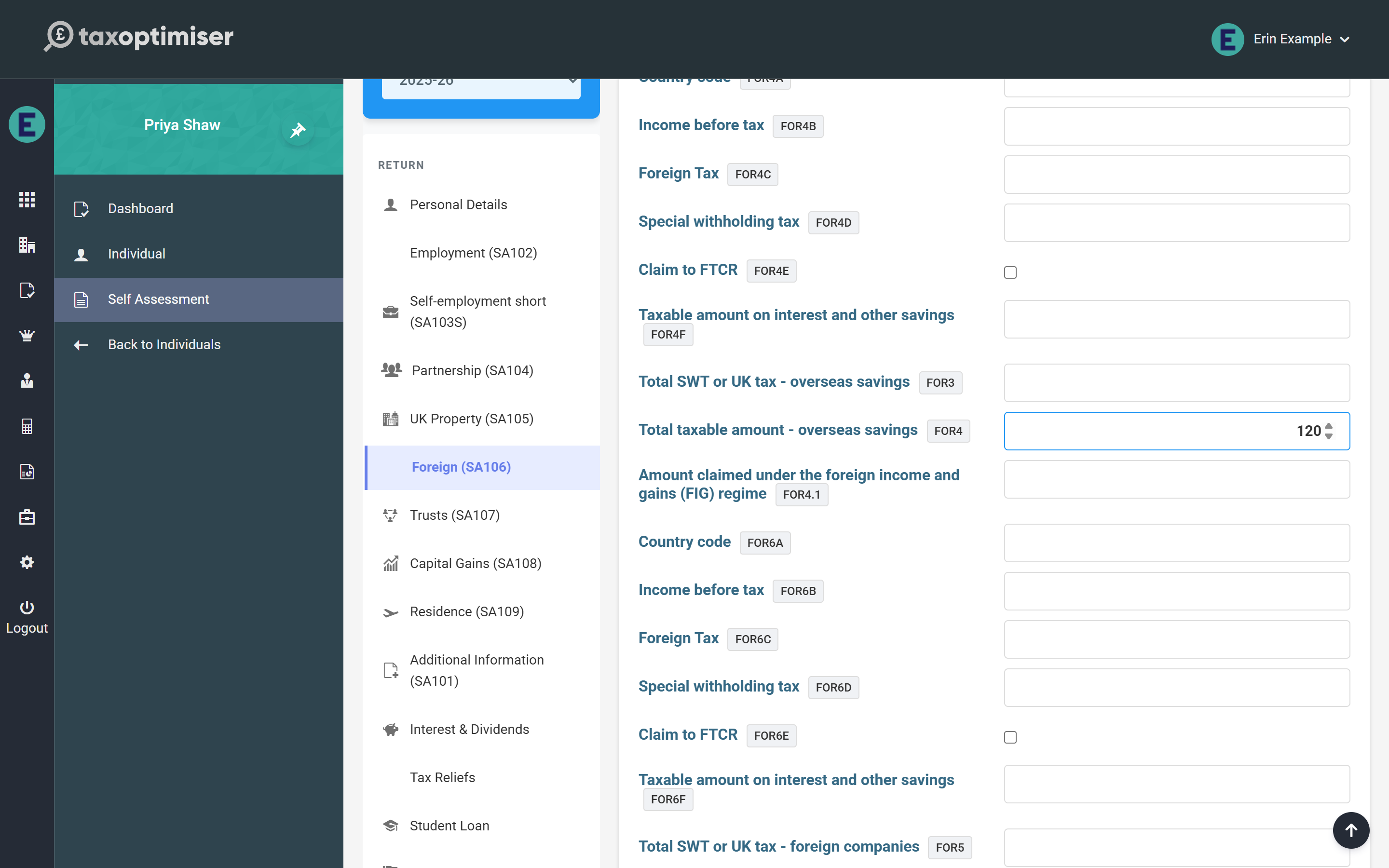

Foreign (SA106)

The foreign page takes the taxable totals by category — overseas savings interest, dividends, pensions, property and other income — together with any special withholding tax or UK tax already accounted for, which is credited like tax deducted at source. Foreign Tax Credit Relief works as it does on the paper form: work out the relief on HMRC’s HS263 working sheet and enter it in box 2; the calculation credits it up to the tax charged and notes that HMRC may recompute it. Overseas residential finance costs earn the same 20% reducer as UK property.

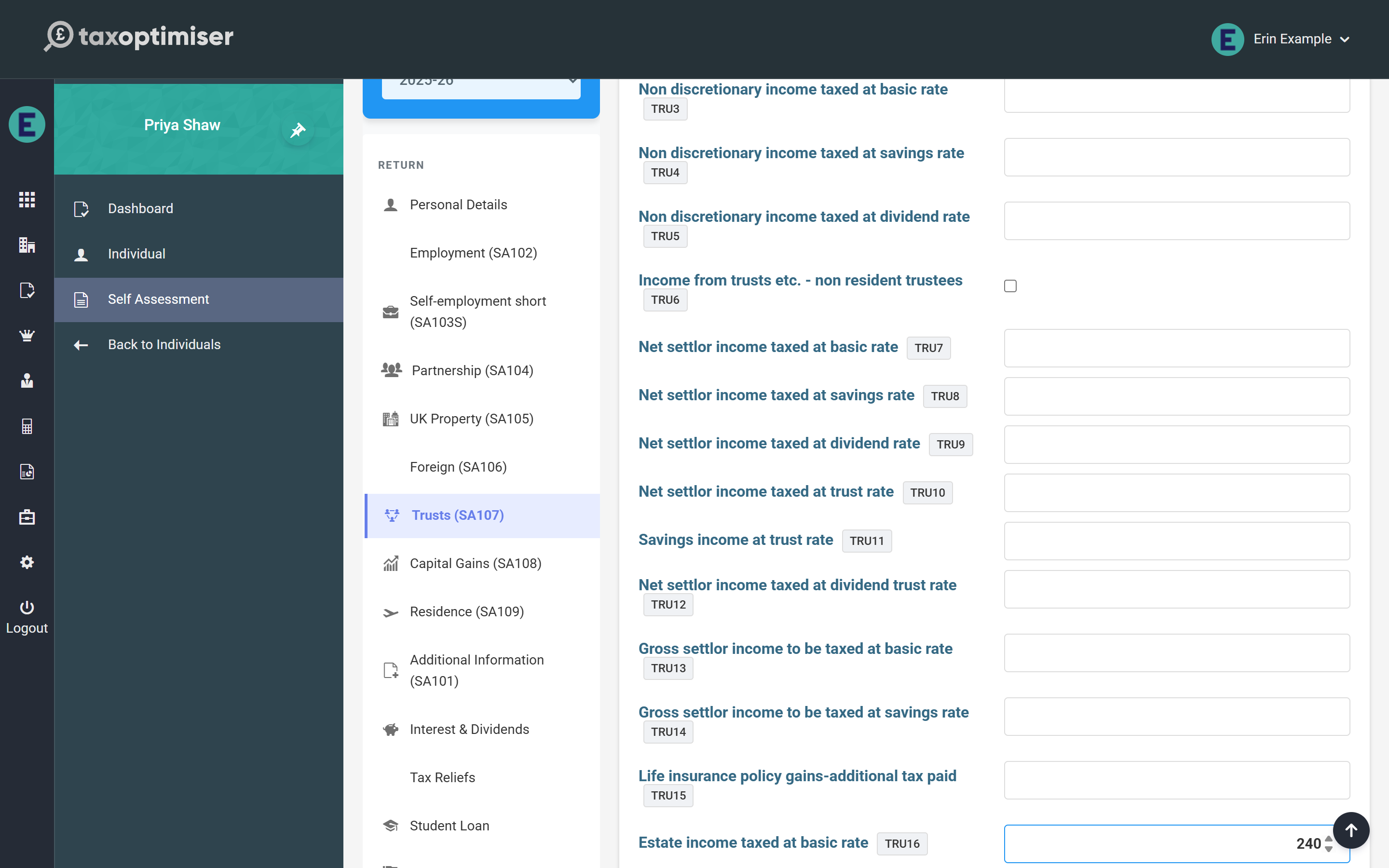

Trusts and estates (SA107)

Enter trust and estate income net, exactly as the R185 shows it — the calculation grosses each box up at the rate the trustees or personal representatives accounted for (basic, savings, dividend or trust rate) and credits the tax automatically. Two credits are non-repayable by law — payments from settlor-interested trusts and estate income taxed at the non-repayable basic rate — and the calculation caps them at the tax due rather than ever creating a refund from them.

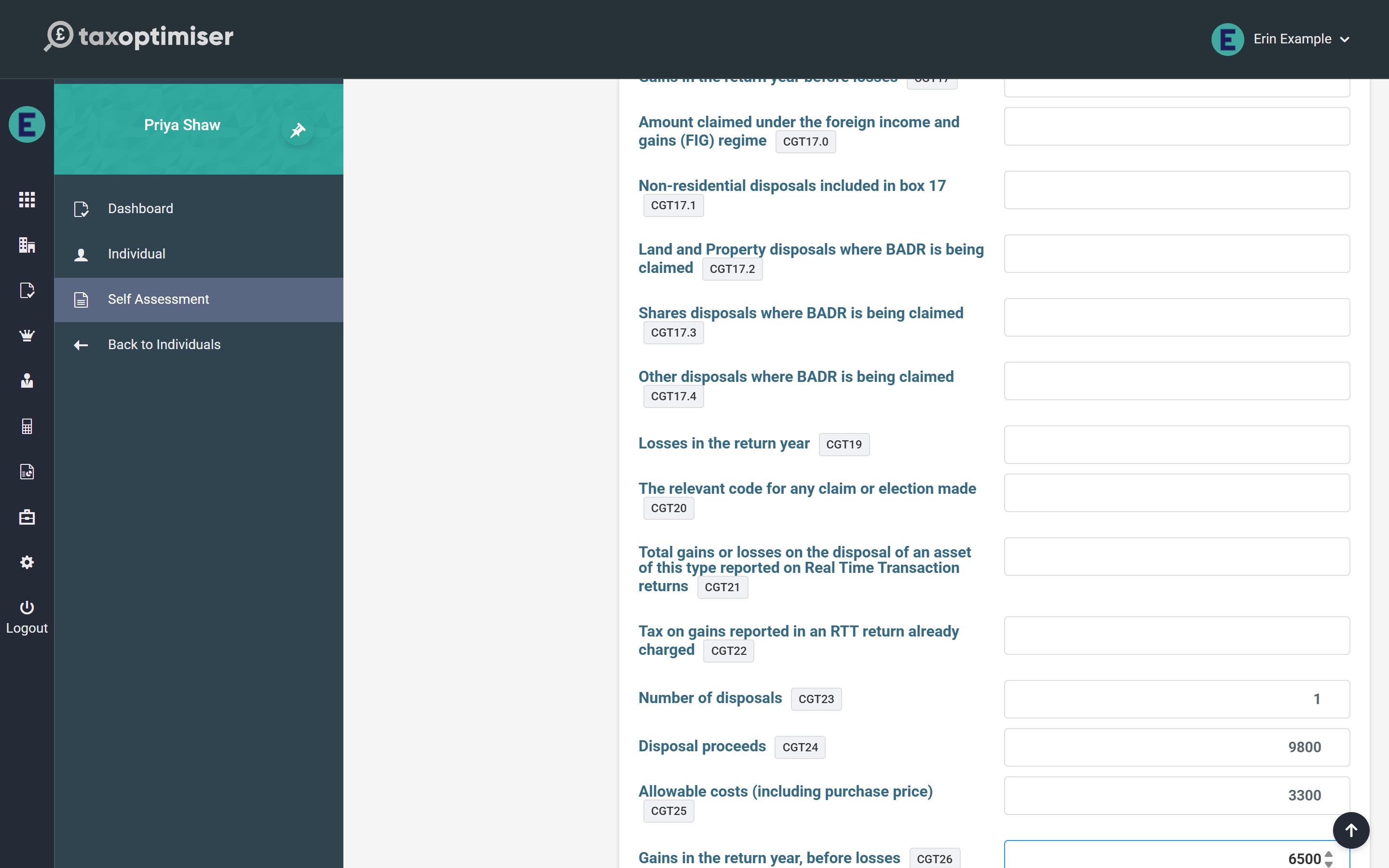

Capital Gains (SA108)

Enter the year’s totals per asset category — residential property, listed and unlisted shares, crypto-assets, other assets — with disposals counts, proceeds, costs, gains and losses, exactly as on the paper form. The calculation applies in-year and brought-forward losses and the £3,000 annual exempt amount, then taxes what remains at 18% within any unused basic-rate band and 24% above it, with Business Asset Disposal Relief and Investors’ Relief gains at their 14% rate and carried interest at its own rate. Tax already charged on in-year property (PPD) or real-time returns is credited against the bill. Capital Gains Tax joins the balancing payment but never the payments on account.

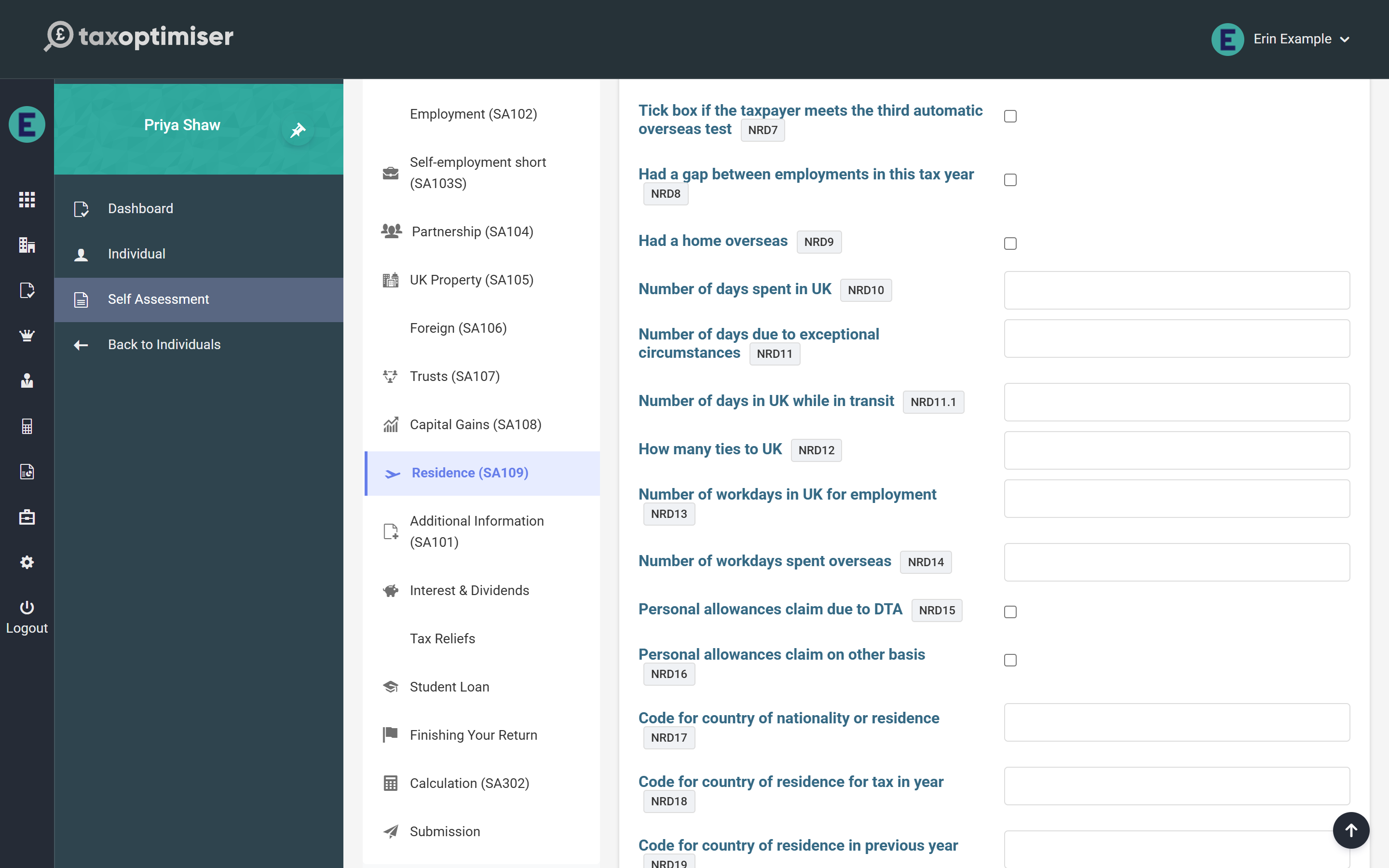

Residence (SA109)

The residence page carries the statutory residence test entries — residence status, split-year treatment, day counts and ties — plus the personal allowance claim boxes. One entry changes the tax directly: a client marked not UK resident loses the Personal Allowance unless boxes 15 or 16 claim it (under a double taxation agreement or another basis), and the calculation shows a note whenever it has removed the allowance.

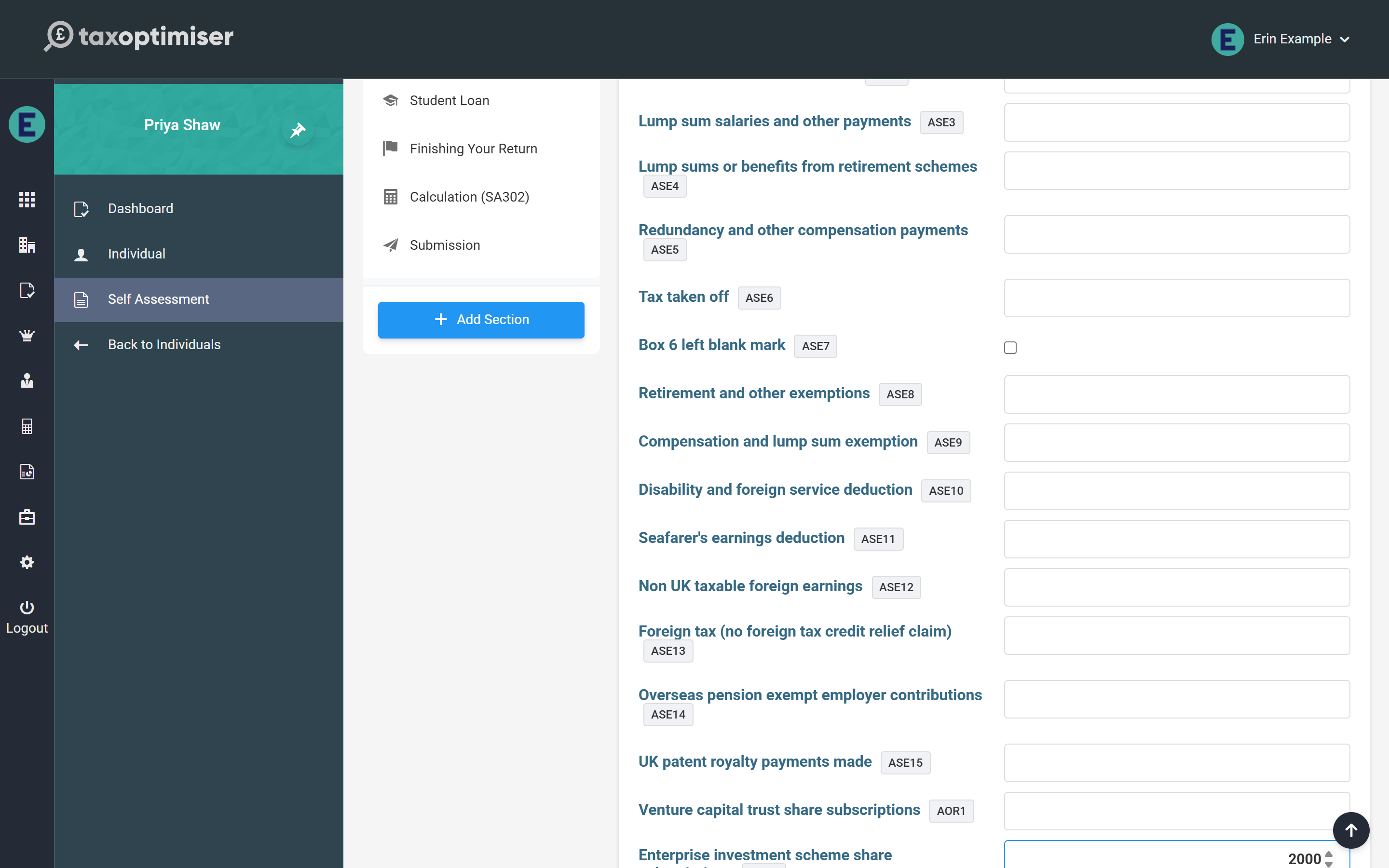

Additional Information (SA101)

The SA101 catch-all page covers the less common entries: gilt interest (entered gross with its tax credited), stock dividends and bonus issues, share schemes and employment lump sums with their exemptions, seafarers’ and foreign-earnings deductions, and the extra reliefs — qualifying loan interest, annuities and, for investments, EIS (30%), SEIS (50%), VCT (30%) and Community Investment Tax Relief, each capped at the tax charged. The age-related Married Couple’s Allowance (a spouse born before 6 April 1935) is worked out here too, with its income taper and transfer options.

What still blocks online filing

A small set of genuinely specialist boxes remains outside the calculation. Using any of them raises a blocking warning on the Calculation section and the pre-flight checks refuse to file, so a wrong self-calculated return can never reach HMRC:

- life-insurance policy gains needing top-slicing relief (SA101, SA106 and SA107 life-gain boxes)

- remittance-basis and foreign income and gains (FIG) regime claims

- non-resident settlor-interested trusts and Transfer of Assets Abroad charges

- double taxation agreement partial relief amounts, Overseas Workday Relief and Temporary Repatriation Facility elections

- non-resident CGT and QAHC/excluded-securities gains

- pension annual allowance and unauthorised payment charges

Returns needing those entries should be filed through other means for now; everything else on these pages files online as normal.